Enterprise Value – Definition and Formulas

You could think of enterprise value as the total price of a company if it were to be bought, from a theoretical standpoint. It’s an excellent tool used by analysts, traders, investors, and journalists of the financial realm to assess an investment case and see if it’s worth it or not, monetarily speaking. From the smallest of firms all the way up to the most valuable company in the world, the giant Apple, here is all you need to know about enterprise value and the way you can calculate it.

No image credit attribution required

What Is Enterprise Value?

As noted in the introduction, enterprise value is considered to be the economic worth of a company. Beyond this theoretical point of view, it’s also a metric used to determine how much an investor or a buyer would have to pay for a particular company if he were to buy it or take over. It also encompasses a company’s debt, which the potential buyer would have to pay as well. However, if this were to happen, the buyer will pocket the extra money.

Enterprise value is different from a plain market capitalization in several capital points. This difference is the reason why many specialists consider it to be better and more accurate when it comes to representing the value of a firm or business.

How to Calculate Enterprise Value

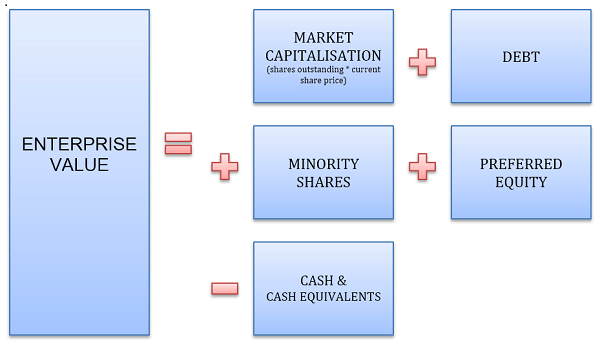

Enterprise value can be calculated using a formula, as follows.

EV = Market Capitalization +Debt +Preferred Share Capital + Minority Interest – Cash and cash equivalents

where

EV = enterprise value

Market capitalization = is the entire market value of all the common shares belonging to a company. It has a formula of its own.

Market capitalization = outstanding shares X share value

A simple example shows us that if a business has 100 000 outstanding shares and each and every one of them is worth $10, the formula indicates that the market cap would then be $1 million.

Debt = is a sum comprised of bonds and bank loans, but not items such as trade creditors. When you purchase a business, all the debts pass into your responsibility. You will also have to repay all the debts from the firm’s cash flows. This will ultimately mean that they will be added to the enterprise value when you calculate it.

Preferred Shares = this type of redeemable shares are considered to be debt as well. Therefore, they are a claim into the business too, which should be taken into account and added to the formula when calculating the enterprise value.

Minority Interest = this is the sum of all subsidiaries owned by the minority shareholders and it is a liability of the non-current type.

Cash and cash equivalents = as the name suggests, this part of the formula revolves around different types of cash, be it simple, cash in hand and cash at the bank. However, it also encompasses all the short-term investments that are considered to be highly liquid and, thusly, easily transformable into cash if the need be.

Make sure you understand that this last value, cash and cash equivalents, must be subtracted from the formula because their purpose is to reduce the price of the acquisition as a whole.

Enterprise Value Seen as a Multiple

An enterprise multiple is one of the ratios employed to calculate how much a company is worth. The concept is one which looks at the business’ value the same way a buyer would do, seeing as it takes debt into account as well, a thing which other multiples do not. The ratio has the following formula.

Enterprise Multiple = Enterprise Value

EBITDA

Following the formula, it’s also called the EBITDA Multiple, where EBITDA stands for earnings before interest, taxes, depreciation, and amortization.

Image credit: Investopedia

Specialists use the enterprise multiple for the following reasons.

- When it comes to transnational comparisons, seeing as it overlooks the twisting effects of the tax policies each country has.

- To locate attractive takeover contenders. If we were to take into account the idea of takeovers, enterprise value is a far better metric than market capitalization. It includes the debt value which the buyer needs to pay when engaging in the transaction. In this way, if a company has a low enterprise multiple, it becomes a real candidate for a takeover.

Tip – enterprise multiples typically differ according to the industry to which they belong. Therefore, you need to compare it to peer companies or the industry as a whole. Industries that are witness to a higher growing rate such as biotech have higher enterprise multiples. The ones that are growing at a slower pace, such as the railways system have lower multiples.

The EBITDA multiple is also related to the fluctuation of free cash flow to the firm, otherwise known as FCFF. From a negative point of view, it’s related to the company’s risk level, as well as to the weighted average cost of capital or WACC.

Here are the drawbacks you need to be aware of regarding the EV/EBITDA.

- In the situation where the working capital grows, EBITDA overstates the cash flow from operations, called CFO or OCF. Even more so, by taking this measure, it will ignore the difference between the revenue recognition policies and how it can affect the firm’s CFO.

- Free cash flow is better related to the valuation theory than to the EBITDA itself. The reason is that it captures the expanse of capital expenditures or CapEx.

How Does It Work? A Practical Example

Building on the above formula, let’s take a look at an example which demonstrates in a practical fashion how to calculate and understand enterprise value.

Once again, the formula, simplified this time is the following one.

Enterprise Value = Market Capitalization + Total Debt – Cash

Image credit: ICMScholars

It’s important to note here that some financial specialists or analysts sometimes adjust the basic formula, especially the debt factor. They proceed in this manner so that the equation can include preferred stock. Some other time, they alter the cash factor as well, exactly as we’ve seen above, in the extended version of the enterprise value mathematical formula. They do this to make sure it includes cash, as well as cash equivalents, such as, for example, accounts receivable or liquid inventories.

Therefore, let’s base our example on a fictional company called Sunflower Furniture. Let’s give it the following financial characteristics.

- 1 000 000 shares outstanding

- 5$ the current price per share

- $1 000 000 summing up the total debt

- $500 000 the total cash amount

Building on our formula here is how the mathematical equation would look if we were to calculate the enterprise value for Sunflower Furniture.

($1 000 000 X $5) + $ 1 000 000 – $500 000 = $5 500 000

As you can well see, the formula is easy to use and user-friendly, once you have mastered the meaning of all its components and factors.

Does Enterprise Value Matter?

Wall Street typically assigns an overall value to a company, and it usually reaches it by looking solely at market capitalization, for which we have provided you with a formula in a segment above. Still, financial analysis has proven that this outlook on things is not sufficient at all, nor is it relevant if one is trying to outline a company’s actual market value.

Enter enterprise value. This metric takes into account a lot more than a company’s outstanding equity and its value. As mentioned above, if you just want to buy a business, you also have to buy its debt but receive its acquired cash. This idea leads to a financial balance. If you purchase the debt as well, it will up the company’s price, but if you receive the cash, it will reduce the cost as a whole.

Cash and debt transform into two crucial elements when it comes to enterprise value if looked upon from this point of view. This is the reason why two companies that have the same market capitalizations could have different enterprise values.

Allow us to give you an example to describe this concept. A company that has a market capitalization of $50 million, no amounted debt, and $10 million in cash, could, in fact, come off as cheaper to purchase than another peer company that has the same market capitalization of $50 million and $30 million in debt.

Errors in Measuring Enterprise Value

If we were to take a look at the standard practices used to measure enterprise value, we could easily spot two problems. One of them is the fact that the formulas mix market, estimated, and book values when taking into account different items. The second one is the fact that all the market values can and are changed at all times while book values, which are based on numbers, are the ones comprised in the last financial statement. Let’s break them down.

#1. Market and Book Value

When attempting to calculate the enterprise value of a company, the sole numbers that the market can provide are those related to market capitalization, as reflected in the market value equity in the common shares. If there are any numbers left, they are provided by accounting statements. As far as debt is concerned, the difference between market and book value will always be small for stable firms and large for problematic ones.

As far as cash goes, value accounting estimates are supposed to be close. Be careful, because trapped cash can be discounted by the market so that it can reflect tax liabilities that are expected.

When it comes to cross holdings, the difference between market and book value usually varies, depending on the time span of the holding. For example, older holdings sport larger differences.

#2. Differences in Timing

Everyone that participates in the big game of investing dreams of their values reflecting present numbers, because, evidently, all investments should reflect current numbers. However, the reality tends to be different, in the sense that only those figures which are market-based can be updated continuously. Therefore, two questions arise from this situation, to which you must find an answer.

- Should you go for uniformity in timing or current value?

- If you choose the latter, what problems will you be facing that will be caused by inconsistencies in the timing factor?

#3. Consistency as opposed to current values

When you turn to value estimates to assess how values have changed over time or why they have varied across different companies as time has passed, then you will find that consistency wins over updating on a regular basis. Therefore, instead of employing the market value of equity as it is at the current moment, you can turn to that of the last financial statement.

If you happen to be using the value estimates so that you can make judgments on investments or transactions at the current moment, the rule of current value is supposed to win. Nonetheless, if you manage to find a business that is cheap, you have an opportunity to purchase it at today’s market price.

#4. Errors coming from inconsistencies in timing

If you feel that you must go with the updated version, then your biggest worry will be related to using data about cash, debt, and several other assets that are estimates. This means that their value may have changed since you saw the last reporting. A company can surely borrow new debt or repay an old one. Either way, the course of action will affect the cash balance. Apart from that, the firm’s operating needs can also cause the cash to either decrease or grow.

It’s clear that enterprise value is a useful metric in a number of situations. Evidently, financial analysts and experts can see and point out its ups and downs, but there is no denying it is crucial when it comes to calculating ratios that will ultimately provide excellent comparisons between peer companies.

Recent Posts

- Forex Indicators: 4 Indicators Investors Should Know

- Best Money Clip: 10 Options to Secure Your Cash

- What is a Savings Account? Explaining Why You Should Have One

- Clarity Money Review: A One-Stop-Shop

- What Do Investment Bankers Do? Ultimate Guide

- Top 10 Best Investing Books

- Best Bitcoin Mining Software: Top 5 Revealed

- Depreciation Methods: Our Top 4 Picks

Leave a Reply